Contents

- 1 How to improve credit score

- 2 Why Your Credit Score Actually Matters More Than You Think

- 3 First, Understand What Actually Goes Into Your Score

- 4 Step 1: Pull Your Free Credit Reports and Actually Read Them

- 5 Step 2: Attack Your Credit Utilization (This Is the Fastest Win)

- 6 Step 3: Fix Late Payments — Even Old Ones

- 7 Step 4: Don’t Close Old Accounts (Even If You Don’t Use Them)

- 8 Step 5: Add Positive Credit If You’re Starting From Scratch

- 9 Common Mistakes That Will Tank Your Score

- 10 Real Timeline: What to Expect

- 11 Tools and Apps I Actually Use

- 12 Frequently Asked Questions

- 13 Final Thoughts

How to improve credit score

How I Went From a 580 to a 740 Credit Score in 14 Months (Here’s Exactly What Worked).

I still remember the embarrassment of sitting across from a car dealership finance manager and watching his expression change when he pulled my credit report. “You’re looking at 19% APR,” he said, sliding the paper toward me. I drove home without the car that day. That moment cracked something open in me — I needed to fix this, and I needed to actually understand how it worked, not just Google “how to raise credit score fast” and hope for magic.

What followed was 14 months of trial, error, a few dumb mistakes, and eventually a real transformation. I went from a 580 FICO score to a 740, and I’ve since helped three family members do the same. This guide is everything I wish someone had handed me that day at the dealership.

Why Your Credit Score Actually Matters More Than You Think

Most people think credit scores only matter when buying a car or a house. That’s wrong.

Your credit score affects:

- The interest rate on your mortgage (a 100-point difference can cost you $50,000+ over a 30-year loan)

- Whether a landlord approves your rental application

- Your car insurance premiums in most U.S. states

- Whether you get approved for a business credit card

- Sometimes even job applications (certain employers check credit)

A 580 score isn’t just “not great.” It’s actively costing you money every single month.

According to myFICO, the difference between a 580 and a 740 credit score on a $300,000 mortgage can mean a difference of over $200 per month in payments. That’s $2,400 per year. Let that sink in.

First, Understand What Actually Goes Into Your Score

Before you try to fix anything, you need to know what you’re fixing. FICO scores — the ones most lenders use — are calculated like this:

| Factor | Weight | What It Means |

|---|---|---|

| Payment History | 35% | Have you paid bills on time? |

| Credit Utilization | 30% | How much of your available credit are you using? |

| Length of Credit History | 15% | How old are your accounts? |

| Credit Mix | 10% | Do you have different types of credit? |

| New Credit (Hard Inquiries) | 10% | Have you applied for a lot of new credit recently? |

When I first looked at my report, I had two late payments from 2021, my utilization was at 78% (brutal), and my oldest account was only 3 years old. No wonder I was at 580.

Understanding this table literally changed how I made every financial decision going forward.

Step 1: Pull Your Free Credit Reports and Actually Read Them

This is where everyone should start. Go to AnnualCreditReport.com — this is the only federally mandated free credit report site. You can now get free weekly reports from all three bureaus (Equifax, Experian, TransUnion). Use it.

When I pulled mine, I found:

- One account listed as “collections” that I didn’t recognize

- A late payment from a medical bill I never knew existed

- An old address that wasn’t mine (minor, but still)

That mystery collections account? Turned out to be a $47 utility bill from an apartment I’d left in 2019. They never sent it to my new address. It was sitting there destroying my score.

What to look for when reading your report:

- Accounts you don’t recognize (possible identity theft or error)

- Late payments that were actually paid on time

- Incorrect balances or credit limits

- Accounts listed as “open” that you’ve closed

- Duplicate accounts

If you find errors, dispute them directly with each bureau online:

- Equifax Dispute Center

- Experian Dispute Center — experian.com/disputes

- TransUnion Dispute — transunion.com/credit-disputes

I disputed that mystery collection account. It was removed within 28 days and my score jumped 31 points almost immediately.

Step 2: Attack Your Credit Utilization (This Is the Fastest Win)

Credit utilization is the ratio of your credit card balances to your credit limits. If you have a $1,000 limit and a $780 balance, you’re at 78% utilization — that’s terrible for your score.

The general rule people throw around is “keep it under 30%.” But honestly? Under 10% is where the real score gains happen.

When I paid my utilization down from 78% to 22%, my score jumped 44 points in a single month. No joke.

Practical ways to lower utilization:

- Pay down balances before your statement closing date (not just the due date — your balance is reported on closing date)

- Ask your credit card issuer for a credit limit increase (without a hard inquiry if possible — just call and ask)

- Open a new card only if you won’t spend on it — this increases total available credit

- If you have multiple cards, spread small balances across them rather than maxing one out

I called Chase and asked for a credit limit increase on my Freedom card. They gave me a $1,500 bump with no hard pull. Instantly my utilization ratio dropped.

A good app to track this in real time is Credit Karma (free) or the Experian app. Both show you your utilization percentage and update regularly.

Apply for a Free Experian Account →

Step 3: Fix Late Payments — Even Old Ones

Payment history is 35% of your score, which makes it the single most important factor.

If you have late payments on your report, here’s what actually works:

Goodwill Letters

This is something most people don’t know about. If you had one or two late payments but have otherwise been a good customer, you can write what’s called a “goodwill letter” — a polite request asking the creditor to remove the negative mark as a gesture of goodwill.

I wrote one to Capital One for a 30-day late payment from 2021. I explained that I’d been dealing with a family emergency, had been a loyal customer for years, and asked if they’d consider removing it. They said yes. It took a single email.

Does this always work? No. But it works more often than people realize, especially with smaller community banks or credit unions.

What if the late payment is accurate and recent?

You can’t erase it, but you can minimize its impact by building a clean payment history on top of it. Over time, older negatives carry less weight. A late payment from 2021 affects your score much less than one from last month.

The most important thing: set up autopay for every account. Every. Single. One. Even if it’s just the minimum payment. You never want another late payment as long as you live.

For more in-depth strategies, the team at FinSaves has put together some of the best plain-English guidance on debt repayment, credit building, and making smart financial moves without needing a finance degree — definitely worth bookmarking if you’re serious about this journey.

Step 4: Don’t Close Old Accounts (Even If You Don’t Use Them)

This one bit me before I knew better.

I had an old store credit card from a furniture shop I never went to anymore. Low limit, no rewards, seemed pointless. I closed it.

Bad move.

Closing it did two things:

- Reduced my total available credit (raised my utilization ratio)

- Eventually shortened my average credit age

Unless a card has an annual fee you can’t justify, leave it open. Use it once every few months on something small — a tank of gas, a grocery run — and pay it off immediately. This keeps it active and helps your average account age.

Step 5: Add Positive Credit If You’re Starting From Scratch

If your credit history is thin or you’re rebuilding from zero, you need to add accounts strategically.

Secured Credit Cards

This is how I helped my younger sister build credit from scratch. A secured card requires a cash deposit (usually $200–$500) that becomes your credit limit. Use it for small purchases, pay it in full every month, and within 6–12 months you’ll have a real credit history.

The Discover it Secured and Capital One Secured Mastercard are consistently rated best-in-class for this.

Apply for Discover it Secured Card →

Credit-Builder Loans

Self (formerly Self Lender) offers credit-builder loans specifically designed to help people establish credit. You make monthly payments into a savings account, and those payments are reported to all three bureaus. At the end, you get the money. It’s basically forced savings plus credit building in one.

Become an Authorized User

Ask a family member or close friend with good credit to add you as an authorized user on one of their old accounts. You don’t even need to use the card. Their positive history gets added to your report.

I did this with my mom’s 12-year-old Visa card. Her perfect payment history on that account boosted my average credit age significantly.

Common Mistakes That Will Tank Your Score

Let me save you some pain.

- Applying for multiple credit cards at once — each application is a hard inquiry that drops your score. Space them at least 6 months apart

- Paying off a collection and expecting a score jump — paid collections still show on your report. Negotiate “pay for delete” before paying

- Closing your oldest account — don’t do it unless you absolutely have to

- Using 0% APT promo cards and forgetting the end date — I’ve seen people get hit with retroactive interest that wrecked both their wallet and score

- Ignoring small medical bills — these quietly go to collections and destroy scores. Check every EOB (Explanation of Benefits) from your insurer

- Thinking checking your own score hurts it — it doesn’t. Checking your own credit is a “soft inquiry” and has zero impact

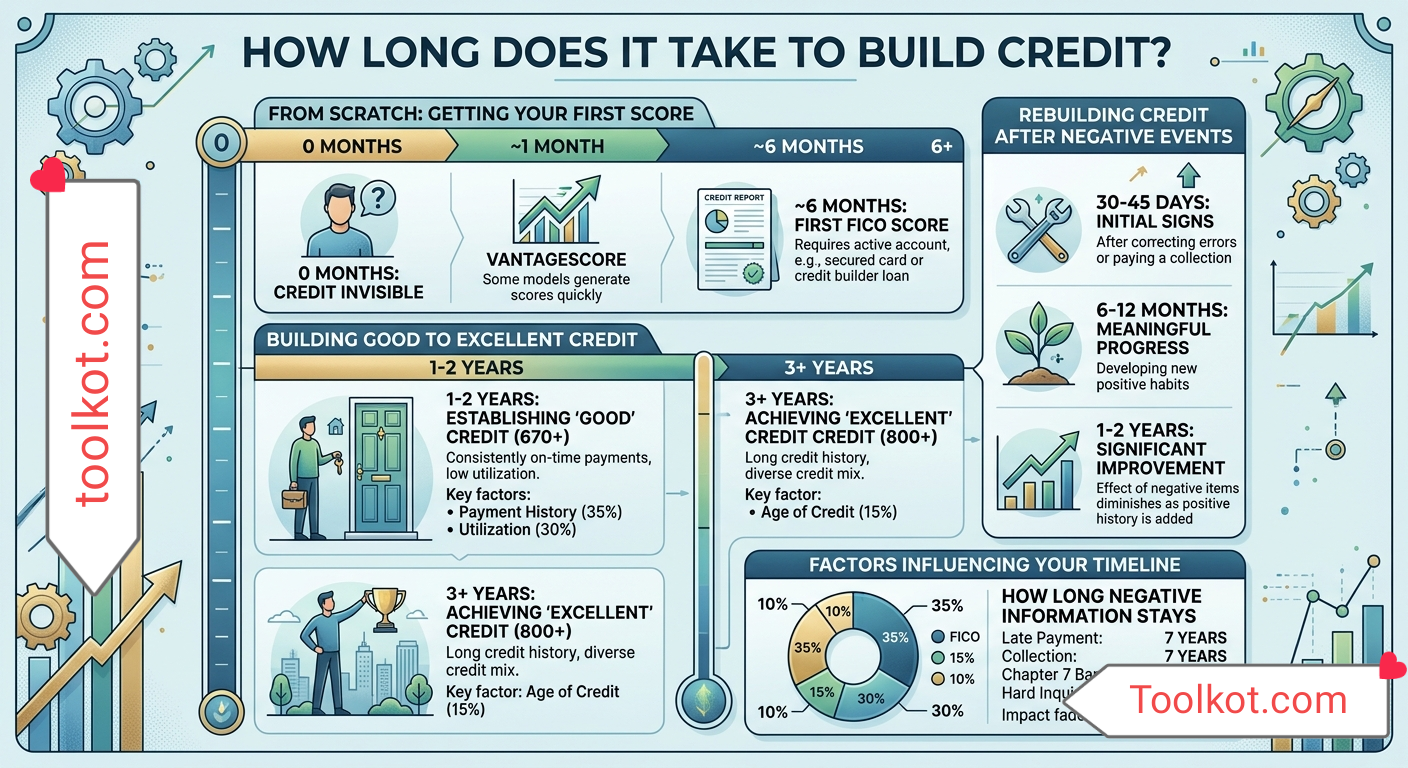

Real Timeline: What to Expect

People want overnight results. Here’s what’s actually realistic:

| Timeframe | What Can Happen |

|---|---|

| 30–60 days | Disputing errors removed; utilization drops show up fast |

| 3–6 months | Payment streak starts helping; authorized user boost visible |

| 6–12 months | Secured card history building; goodwill removals show effect |

| 12–24 months | Significant score movement if you’ve been consistent |

There’s no shortcut that works without eventually wrecking something else. Credit repair companies that promise “100-point increase in 30 days” are either lying or about to do something that will create bigger problems later.

According to Consumer Financial Protection Bureau (CFPB), legitimate credit improvement takes time and consistent positive behavior — no company can legally remove accurate negative information from your report.

Tools and Apps I Actually Use

- Credit Karma — Free score monitoring, utilization tracker, dispute guidance

- Experian App — Shows FICO Score 8, real-time alerts, Experian Boost (adds utility/streaming payments to your report)

- Self App — Credit-builder loan management

- Mint or YNAB — Budgeting so you never miss a payment again

- AnnualCreditReport.com — The only official free report site; don’t use any other

Frequently Asked Questions

How long does it take to improve a credit score?

It depends on what’s hurting your score. Disputing errors can move the needle in 30 days. Building consistent payment history takes 6–18 months for meaningful improvement.

Will checking my credit score hurt it?

No. Checking your own score is a soft inquiry and has zero impact. Only hard inquiries (from lenders when you apply for credit) can temporarily lower your score.

Does paying off debt immediately improve my score?

Paying down credit card balances (especially high-utilization cards) can improve your score within one billing cycle. Paying off installment loans (car, student) has a smaller immediate effect.

Can I really dispute errors on my credit report?

Absolutely. The Fair Credit Reporting Act gives you the legal right to dispute any inaccurate information. Bureaus are required to investigate within 30 days.

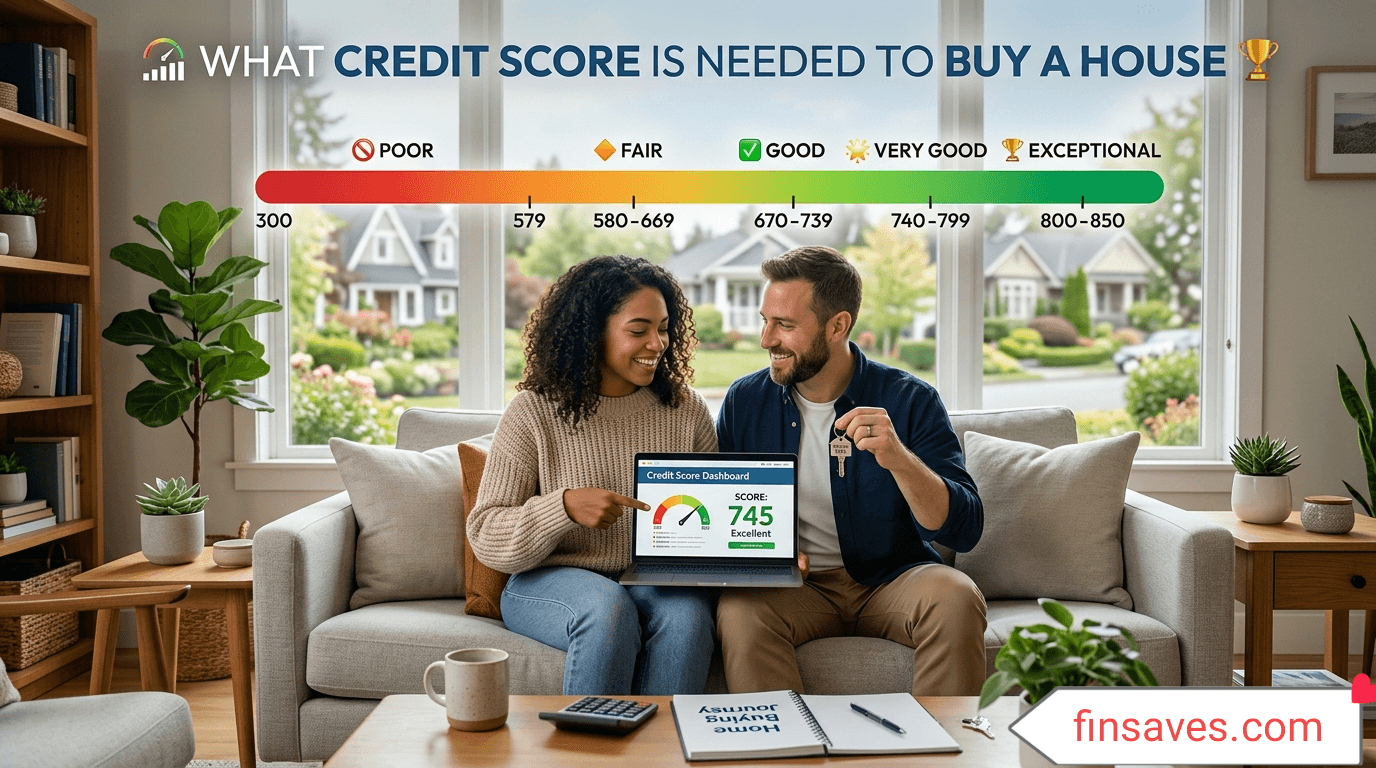

What’s a good credit score to aim for?

760+ gets you the best rates on virtually every financial product. 700–759 is still very good. 670–699 is average and you’ll qualify for most things. Under 670 and you start paying more.

Should I pay for a credit repair company?

Almost never. Everything they can legally do, you can do yourself for free. The CFPB has documented numerous cases of credit repair scams. Save your money.

Does Experian Boost actually work?

Yes — for Experian scores specifically. It lets you add on-time utility, phone, and streaming payments to your Experian credit file. I saw a 19-point boost when I connected it. Results vary, but it’s free and takes 5 minutes.

Final Thoughts

The day I got approved for a car loan at 6.9% APR — down from the 19% I’d been quoted 14 months earlier — I genuinely teared up a little. It wasn’t just about the money, though saving $4,000 in interest over the life of the loan was great. It was the feeling of being in control of something that had felt completely out of reach.

Your credit score is not a judgment of your worth as a person. It’s a number built from data — and data can be corrected, improved, and rebuilt. All it takes is knowing which levers to pull and being patient enough to let them work.

Start with your free credit report today. Find one thing to fix this week. One.

That’s how every real turnaround story begins.

For more practical, jargon-free guides on personal finance, credit building, and making smarter money decisions, visit FinSaves.com — it’s the kind of resource I wish existed when I was sitting in that car dealership.

Sources and References:

- myFICO Loan Savings Calculator — myfico.com

- Consumer Financial Protection Bureau — consumerfinance.gov

- AnnualCreditReport.com — federally mandated free credit report portal