Contents

- 1 How Long does it Take to Build Credit

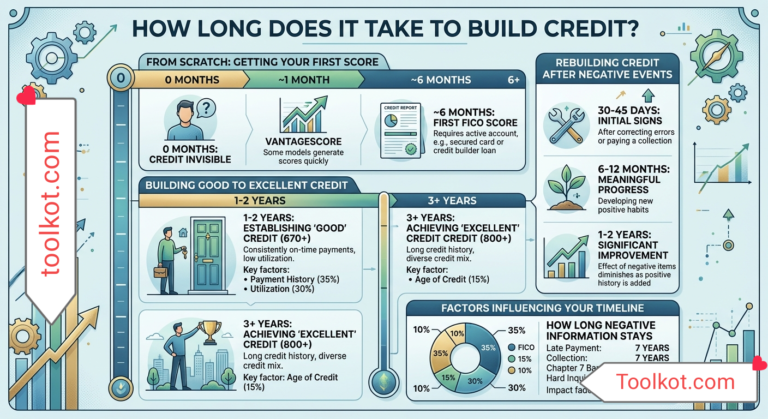

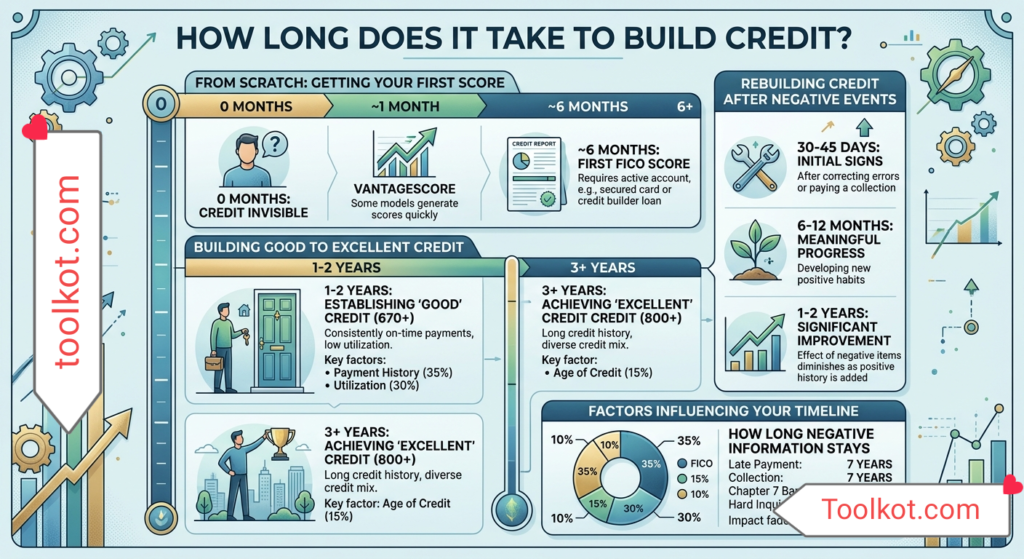

- 2 The Short Answer: How Long Does It Actually Take?

- 3 The Month-by-Month Credit Building Timeline

- 4 The Formula: What Actually Makes Up Your Score?

- 5 The Biggest Mistake I Made: Misunderstanding Utilization

- 6 3 Modern Tools That Actually Work to Build Credit

- 7 Common Myths That Need to Die

- 8 Frequently Asked Questions (FAQs)

- 9 The Bottom Line on Your Credit Timeline

- 10 About the Author

How Long does it Take to Build Credit

A few years ago, I found myself sitting in a leasing office, staring blankly at a property manager who had just denied my apartment application. I had a solid job, money in the bank, and zero debt. But I also had a “ghost” credit profile. I had never opened a credit card, assuming that paying for everything in cash was the smartest financial move I could make.

I quickly learned that in the eyes of lenders, landlords, and even cell phone providers, having no credit is often treated the exact same as having bad credit.

That day, I went home, opened my laptop, and aggressively searched for a magic button to fix it. I applied for my first secured credit card, bought a cup of coffee with it, and immediately checked my banking app. Nothing. A week later, still nothing.

If you are frantically checking your credit monitoring app waiting for a number to finally appear, I know exactly how you feel. The waiting game is frustrating. But the truth is, the timeline to build credit isn’t a mystery—it is built on a very specific mathematical formula used by the major credit bureaus.

Here is exactly how long it takes to build credit, the exact timeline you can expect, and the mistakes I made along the way that you should absolutely avoid.

The Short Answer: How Long Does It Actually Take?

The time it takes to see your first credit score depends entirely on which scoring model you are looking at. There are two major players in the game: FICO and VantageScore.

If you are starting from absolute scratch, it takes exactly six months to generate your first FICO score.

However, you might see a VantageScore pop up in your banking app or a free credit monitoring service in as little as one to two months.

Why the massive difference? It comes down to the rules each company sets for their algorithms.

VantageScore was created collaboratively by the three major credit bureaus (Equifax, Experian, and TransUnion). Their system is designed to score people faster. As soon as you open an account and the lender reports your very first billing cycle to the bureaus, VantageScore can generate a number.

FICO, on the other hand, is the industry heavyweight. Created by the Fair Isaac Corporation, FICO scores are used by about 90% of top lenders. Whether you are buying a car or a house, the lender is almost certainly pulling your FICO score.

To generate a FICO score, your credit file must meet two strict requirements:

- You must have at least one account that has been open for six months or longer.

- You must have at least one account that has been reported to the credit bureaus within the past six months.

Because FICO is the score that actually matters when you want to borrow money, you should mentally prepare yourself for a six-month journey.

The Month-by-Month Credit Building Timeline

When I got my first secured card, I drove myself crazy because I didn’t understand how billing cycles worked. I thought the day I swiped the card was the day the credit bureaus knew about it. That is not how the system operates.

Here is what the real timeline looks like when you open your first account.

Month 1: The Setup and the Silence

You apply for a starter card. Let’s say you get approved on March 1st. You make a small purchase on March 5th.

Your credit card issuer operates on a roughly 30-day billing cycle. They will not send any data to the credit bureaus until your statement closes. For the entire first month, your credit report will remain completely blank.

Month 2: The First Data Drop

Your first statement closes in early April. A few days later, the card issuer sends that data to Equifax, Experian, and TransUnion.

At this point, if you log into a free credit monitoring app, you will likely see your very first VantageScore. It might not be a massive number, but it is a start. However, if you apply for a car loan today, the dealer will tell you that you still don’t have a score, because your FICO is still locked.

Months 3 to 5: The Consistency Test

This is the boring part. You need to keep using the card for small, everyday purchases. More importantly, you need to pay the bill perfectly on time. Every month, the card issuer updates the bureaus. Your VantageScore might fluctuate by a few points, but you are primarily just laying the foundation.

Month 6: The FICO Reveal

You finally cross the six-month threshold. Your first FICO score is officially generated. If you have kept your balances low and made every payment on time, you can expect your debut FICO score to land somewhere in the high 600s or low 700s—which is considered “Good” credit. You are now officially on the map.

The Formula: What Actually Makes Up Your Score?

Understanding the timeline is only half the battle. You also need to know exactly what the algorithm is grading you on.

When I first started, I thought the amount of money I made influenced my credit score. It doesn’t. Your salary, your bank account balance, and your debit card usage have absolutely zero impact on your FICO score.

Here is a breakdown of what actually matters.

| Scoring Factor | Weight | Plain English Translation |

|---|---|---|

| Payment History | 35% | Do you pay your bills on time? A single 30-day late payment can destroy your score for years. |

| Amounts Owed (Utilization) | 30% | How much of your available limit are you using? Lower is always better. |

| Length of Credit History | 15% | How long have your accounts been open? This is why it takes time to reach the 800 club. |

| Credit Mix | 10% | Do you have different types of credit? (e.g., a credit card plus an installment loan). |

| New Credit | 10% | Are you opening too many new accounts all at once? This makes lenders nervous. |

The Biggest Mistake I Made: Misunderstanding Utilization

Let me save you from the exact mistake that tanked my score during my first year.

My first secured credit card had a limit of $300. I thought, “Great, I have $300 to spend!” So, I used it to buy groceries and gas, racking up a balance of $250. I paid it off in full on the due date, assuming I was being a responsible adult.

The next month, my score plummeted. Why? Because of Credit Utilization.

Utilization is the percentage of your total credit limit that you are currently using. The credit bureaus don’t look at whether you paid the bill off after the statement closed; they look at the balance that gets reported on the day the statement closes.

Because I spent $250 out of my $300 limit, my utilization was 83%. Lenders view high utilization as a sign of financial panic. The golden rule is to keep your utilization under 30%. But if you want the absolute highest score possible, you need to keep it under 10%.

My current strategy: If I have a $300 limit, I only put a $10 Netflix subscription on the card. I set it to autopay and throw the card in my desk drawer. It reports a tiny 3% utilization every month, which the algorithm absolutely loves. If you want to dive deeper into managing your daily budget to ensure you never overspend your limits, I highly recommend checking out some of the advanced tracking methods over at FinSaves, which completely changed how I look at personal cash flow.

3 Modern Tools That Actually Work to Build Credit

Back in the day, your only option was a secured credit card. Today, the financial tech space has exploded with brilliant tools designed specifically to help you build a profile from scratch without going into debt.

1. Credit Builder Loans

Apps like Self and Kikoff have revolutionized this space. Instead of giving you money upfront, a credit builder loan places the funds into a locked savings account. You make small monthly payments (like $25 a month), and the app reports these as on-time installment loan payments to the bureaus. Once the term is up, the locked money is returned to you. It forces you to save money while simultaneously building a solid payment history.

2. Rent and Utility Reporting

For years, you got zero credit for paying your rent on time, which is completely unfair. Now, you can use a tool like Experian Boost to connect your bank account and get credit for your Netflix, Hulu, cell phone, and utility payments. It is completely free and can artificially bump your score by a few points almost instantly by adding positive data to your Experian file.

3. Secured Credit Cards with No Hard Pull

A hard pull is when a lender checks your credit, which temporarily drops your score by a few points. If you have no credit, you want to avoid hard pulls. Companies like Chime and Discover offer excellent secured cards that do not require a traditional hard credit check. You deposit your own money, which becomes your credit limit, making it a perfectly safe sandbox to build a history.

Apply Online Here ➔ (Check with your preferred banking app to see their current secured card offers).

Common Myths That Need to Die

There is a lot of terrible advice floating around the internet. Let’s clear up a few things.

- Myth: You need to carry a balance to build credit.

Fact: This is the most expensive lie in personal finance. You do not need to pay a penny in interest to build a perfect credit score. Pay your statement balance in full, every single month. - Myth: Checking your own credit hurts your score.

Fact: Checking your own score is considered a “soft pull” and has zero impact on your credit. You should be checking it regularly. You are legally entitled to free weekly reports from all three bureaus at AnnualCreditReport.com. - Myth: Closing an old card will help my score.

Fact: Closing your oldest account shortens your average age of credit and lowers your total available credit limit. Unless the card charges an exorbitant annual fee, buy a pack of gum with it once a year to keep it open.

Frequently Asked Questions (FAQs)

Can I build credit in 30 days?

No. You might generate a preliminary VantageScore in 30 to 60 days, but you will not have a widely accepted FICO score or a deep enough history to qualify for major loans. Building trust takes time. Expect a 6-month minimum commitment for real results.

How long does it take to rebuild bad credit compared to starting fresh?

Rebuilding is significantly harder and takes longer than starting from scratch. Late payments and charge-offs remain on your credit report for seven years. While their impact lessons over time, it can take 12 to 24 months of perfect payment history to start burying those negative marks and see a meaningful score increase.

Do I need a credit card to build credit?

Not necessarily, but it is the fastest and easiest route. If you are entirely opposed to credit cards, you can use a credit builder loan or have a trusted family member add you as an “authorized user” on their oldest, perfectly paid credit card. You inherit their good history without ever needing to touch the physical card.

What happens if I miss a payment during my first six months?

It is catastrophic for a new credit profile. Because your file is so “thin,” a single 30-day late payment will plunge your new score into the sub-prime category. Always set up autopay for at least the minimum balance to ensure you are never late.

The Bottom Line on Your Credit Timeline

Building credit is a lot like planting a tree. You can’t yell at a seed to make it grow faster. You just have to water it, make sure it gets sunlight, and let time do the heavy lifting.

The six-month wait for your first FICO score might feel like an eternity when you are eager to buy a car or rent your dream apartment. But if you take this time to automate your payments, keep your utilization microscopic, and avoid applying for random store cards, you will cross that finish line with a score that opens doors instead of slamming them in your face.

Don’t overcomplicate it. Pick a low-risk starter tool, spend $10 a month on it, pay it off immediately, and go live your life. The algorithm will take care of the rest.

Have you recently started your credit-building journey? Drop a comment below and let me know which starter card or app you decided to go with—I’m always testing new tools and would love to hear what is working for you right now.